news

Indian startup funding falls by 76% from Jan to Jul 2022 - Funding winter strikes hard

Wed Aug 24 2022

5 min read

techadmin

Startups across stages and high-burn companies are still pacing through the chilly wave of a “funding winter” where uncertainty around equity-backed funding is shaking things up for founders across industries. Between January and July 2022, startup funding has reduced by 76%, going down from $4.6 Bn in January to $1.11 Bn in July, as per Inc42. It is not the first time global public markets are plummeting & entrepreneurs are riddled with questions about how to make it past this without needing more cash to solve their problems. After raising record funds in 2021, Indian startups are struggling to raise money as they see investors rescind offers at the last minute. Our team spoke with over 300 entrepreneurs across growth stages and there was one round-the-clock question:

“What should we do to extend our businesses’ runway?”

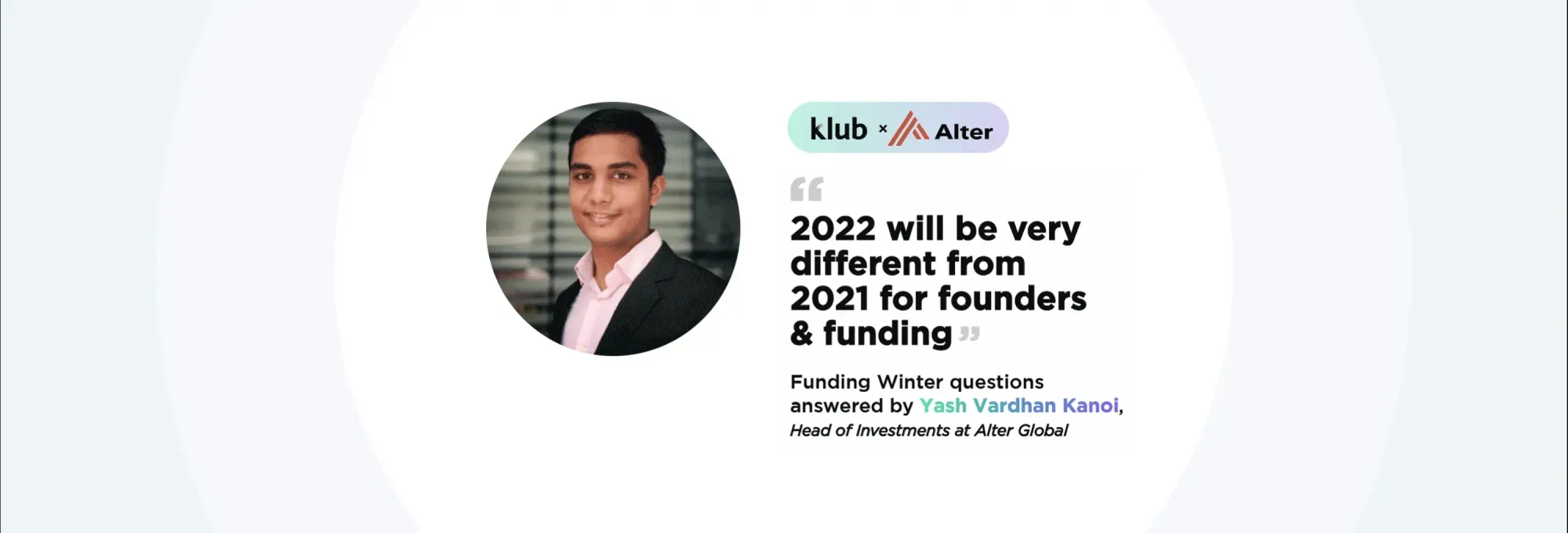

To answer this question, we spoke to the industry expert, Alter Global’s Head of Investments, Yash Vardhan Kanoi and here is what he has to say.

Q1. What should founders expect from this funding slowdown and what is your take on this after the last two years when we saw unicorns at the speed of light?

Yash - So the current market has a far greater concentration on unit economics. The evaluation process is a little bit more rational than it used to be, maybe last year or the year before. Now, a really considerable time is going into due diligence of the companies, which to be honest is a great thing in my opinion. Last year, we saw rounds being closed in two or three days or maximum a week, where the whole idea of FOMO investing really kicked in, right? But that's not happening so much anymore. Eternally, I still believe that great founders will continue to get access to capital, even if it is the so-called “funding winter”.

As David Sacks from Craft Ventures put it, “Companies which are default investable, companies which really have that unit economics to raise another round with low burn multiples, will continue to attract capital.” The market is likely to get consolidated is what we think. And founders which have access to resources could actually capitalize on the same. Throughout 2021, the valuations were on the higher side. There were times when we saw five companies do the exact same thing, in the same region, solved the exact same problem, and all of them got funded. That is something that we probably would not see this year. Again, the period of high burn and high growth is over. 2021 was a liquidity-driven rally produced by excess money printed in the ecosystem. And that has to be honestly funnelled out. This is exactly what we are seeing now that asset prices are getting normalized.

Q2. There's also a lot of conversation around revaluations. What is your opinion on that?

Yash - I think it depends on the stage. So according to evaluations, a lot of what is going on right now is actually evaluation repricing. We see a lot more of them happen in later stages because they are closer to the public markets. We've seen the evolution that big tech and the public markets have seen in the past six months.

Fundamentally, as Alter Global, we are early-stage investors, which is Seed, Pre-seed and up to Series A. Those numbers and those valuations are fairly been insulated because founders who are building at that stage are building for like four, six, eight years. But I do think that at some point, based on the multiples at which companies were getting valued now, investors are being deep rather than just seeking vanity metrics. They’re actually going into net revenue and contribution margin level numbers, which will obviously have an after effect on the valuations.

As Alter, we are continuing to invest across emerging markets because we truly believe that it's a great time to build. Lower competition, better access to talent and frankly, even companies who are building right now are building with better unit economics in their mind. That's what we are kind of seeing here & not in the saturated markets we operate in.

Q3. What is your viewpoint on how companies should extend their runway in order to survive through the Funding Winter?

Yash - This is something that we are actually helping and advising a lot of our portfolio companies on. I would say 70% of our time is actually being spent now helping and focusing on our portfolio companies. Some suggestions we offer to founders building these brands are:

a. Being laser-focused on core business drivers and really doubling down on that. Like in 2021, we saw a lot of experiments being taken into a lot of adjacent markets, which is okay at that point in time. But now, since capital is a bit scarce, we really have to look and double down on the core metrics. Thinking about customer retention more than ever by elevating the customer experience.

b. Ensuring & rechecking the productivity of the team. Because founders will have to ensure that the ROI per employee is justified from a business PoV. If it isn’t, then actions need to be taken to bridge this gap.

c. Corporate governance standards to be of the highest order because there are critical decisions which need to be taken. These include the really hard ones on letting employees go or the critical ones like evaluating an acquisition offer.

d. And then lastly, I do think that looking at alternative funding options, like invoice discounting & revenue-based financing can help founders with liquidity which translates to extending the runway for cash-flow positive brands. These options deserve a worthy evaluation to deal with challenges which probably didn’t exist in the market five or six years ago.

Q4. Exceptional brands and products have thrived through the 2008 global recession and are today giants in their own fields. Keeping that in mind, what is your piece of advice to entrepreneurs to deal with the current phase?

Yash - Indian startups have ****performed exceedingly well in the last decade, even putting the whole country on the world map. Given all the probabilities, there are a lot of opportunities which will come out while we are trying to come out of this phase. One of the things we've seen often is brands doubling down on core SKUs and being more thoughtful around non-essential spending and processes.

For example, the popular US retailer Costco. Early on during the 2008 recession, they reduced the number of product variations from 600 SKUs to 3700. This move allowed Costco to steadily grow their revenues and actually thrive beyond the recession. Brands need to make sure they are spending on products they can earn from instead of acting on their vain ambitions.

Number two, and this is something we'll see more often, given the market remains super flexible on the business model. There's a lot of convergence brands need to do in order to come out as a segment leader post the market slowdown. A brand may have to readjust the business model or its product to ensure that it's successful in the long term. One of the examples that I can think of is Warby Parker. It was founded in the middle of the recession and the brand really capitalised on customers’ reduced spending by offering stylish quirky eyewear at a below-market price point. One challenge for them was a stagnant cost structure. To reduce the shipping costs, they decided to experiment with virtual try-on technology. And when they did that they really found an adjacent need in digital eye exams, opening up a whole new market. For some industries, founders may need nimble pivoting and for others, learning through different technology-driven disruptions like Warby Parker is going to be game-changing.

In my opinion, just like brands, even the market is different as compared to 2008. One of the key differences between 2008 & now is the existence of platforms like Klub where founders have access to alternative ways of financing. I would say, when the equity market is playing wait and see, a brand can easily take advantage of platforms like Klub to get ahead of the curve.

If any of this seemed like a relatable problem with a helpful solution, join the Klub here.

checkout more great content

Wed Oct 08 2025

1 min read

Resilient SMEs treat debt as a strategic asset: planned, measured, diversified, and optimized over time. Healthy founda...

Wed Oct 08 2025

1 min read

Beyond bank loans, UAE businesses can tap flexible capital from alternative sources—useful for e-commerce and retail. P...

Wed Oct 08 2025

1 min read

Debt becomes a problem when payments are hard, covenants break, or new funding is unavailable. Early action keeps option...

Wed Oct 08 2025

1 min read

UAE peaks: Ramadan/Eid, DSF, back-to-school, National Day, winter tourism. These bring high demand and higher costs befo...